Introduction The Union Budget 2026-27, presented by Finance Minister Nirmala Sitharaman, has ushered in significant procedural changes under the proposed Income Tax Act, 2025. With a clear focus on “Ease of Living” and reducing compliance friction, the government has overhauled the timelines for filing Income Tax Returns (ITR).

For taxpayers—ranging from salaried individuals to MSMEs—understanding these new due dates is crucial to avoid penalties and ensure smooth compliance. Here is a breakdown of the critical changes regarding Normal, Belated, Revised, and Updated returns.

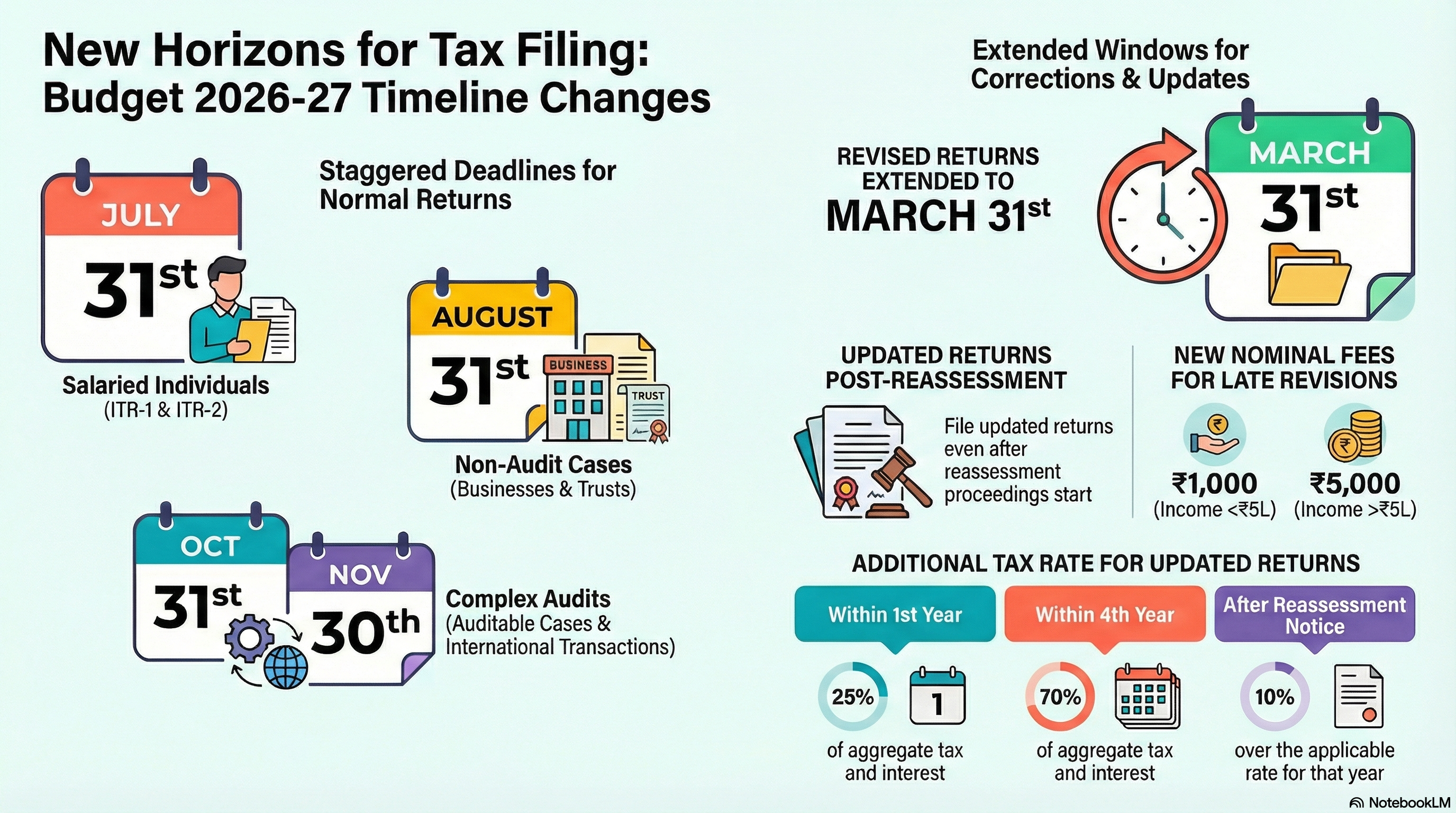

1. Staggered Due Dates for Normal Filing (Section 139 / Section 263 of New Act)

In a move to decongest the portal and provide businesses more time for book-keeping, the Budget proposes staggering the filing timelines based on the nature of the taxpayer.

- Salaried Individuals (ITR-1 & ITR-2): There is no change for individuals filing simpler forms. The due date remains 31st July of the assessment year.

- Non-Audit Business Cases & Trusts: A significant relief has been provided here. For assesses having income from business or profession whose accounts are not required to be audited (and partners of such firms), the due date has been extended from 31st July to 31st August.

- Audit Cases: For companies and assesses requiring tax audits, the date remains 31st October.

- Transfer Pricing Cases: For cases involving international or specified domestic transactions (Section 172), the date remains 30th November.

2. Extended Timeline for Revised and Belated Returns

Perhaps the most taxpayer-friendly procedural change is the extension of the window to fix errors or file late returns.

- New Deadline: Previously, the deadline for filing a Revised Return (to correct errors) or a Belated Return (late filing) was 31st December. This has now been extended to 31st March of the relevant Assessment Year.

- The Catch (Nominal Fee): While you now have three extra months (Jan-March), filing a revised or belated return during this extended period (after 31st December) will attract a nominal fee. The fee structure is proposed as ₹1,000 or ₹5,000, depending on whether the income is up to or more than ₹5 lakh.

3. Updated Returns: Relief During Reassessment

The Budget has introduced a mechanism to reduce litigation by allowing taxpayers to “come clean” even after scrutiny has begun.

- Filing After Reassessment Notice: Taxpayers will now be allowed to file an Updated Return even after reassessment proceedings have been initiated (i.e., after the issuance of a notice under Section 148/Section 280).

- Additional Tax Cost: To utilize this facility, the taxpayer must pay an additional 10% tax rate over and above the rate applicable for the relevant year.

- The Benefit: Filing an updated return under these circumstances and paying the additional tax will grant the taxpayer immunity from penalty on that additional income. The Assessing Officer will then use this updated return for the proceedings.

Summary of New Timelines

| Return Type | Category of Taxpayer | Old Due Date | New Due Date (Proposed) |

|---|---|---|---|

| Normal | Individuals (ITR 1 & 2) | 31st July | 31st July (No Change) |

| Normal | Business (Non-Audit) & Trusts | 31st July | 31st August |

| Revised / Belated | All Taxpayers | 31st December | 31st March (With Fee) |

Disclaimer: The content above is based on the proposals contained in the Finance Bill, 2026 and Budget documents. These provisions are subject to the passing of the Bill in Parliament.