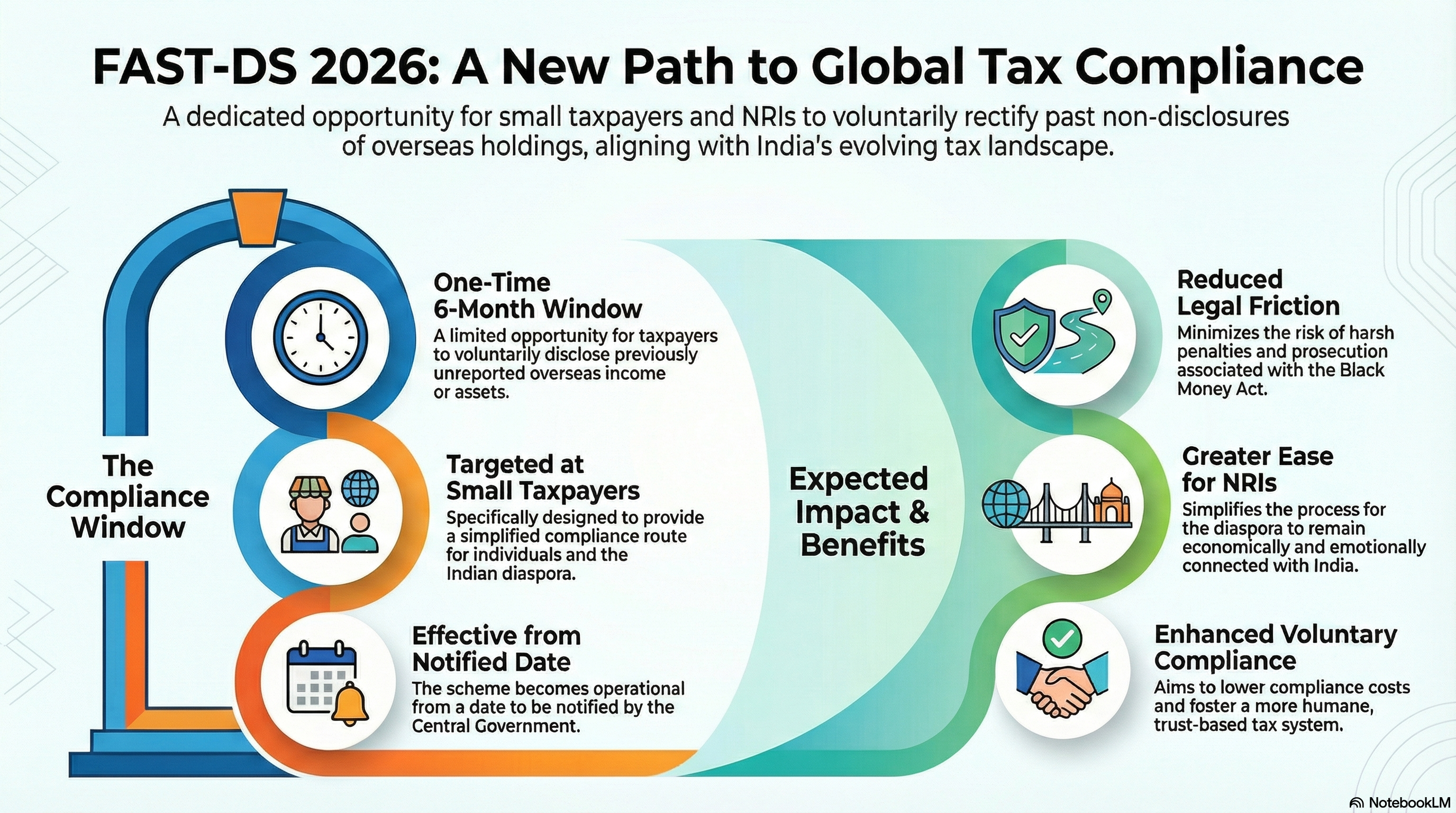

Introduction One of the most significant relief measures in the Union Budget 2026-27 is the introduction of the Foreign Assets of Small Taxpayers – Disclosure Scheme, 2026 (FAST-DS 2026). Designed to end “tax terrorism” for small taxpayers, this one-time compliance window targets individuals who inadvertently failed to disclose foreign assets—such as employees with ESOPs, students with dormant foreign bank accounts, or professionals who have returned to India.

The scheme acknowledges that many small taxpayers failed to report foreign assets not out of malicious intent, but due to a lack of awareness regarding the stringent reporting requirements of Schedule FA in income tax returns.

Who is FAST-DS 2026 For?

The government has explicitly designed this scheme to resolve legacy issues for small taxpayers. It specifically targets:

• Tech Employees: Holding Employee Stock Options (ESOPs) or Restricted Stock Units (RSUs) in foreign parent companies,.

• Students: Who may have opened bank accounts while studying abroad and left them dormant with low balances upon returning to India,.

• Relocated NRIs: Individuals who have returned to India and retained savings or insurance policies abroad,.

Scheme Structure: Two Categories of Relief

The scheme, proposed to be open for 6 months,, categorizes non-compliant taxpayers into two distinct groups based on the nature of their default.

Category A: Undisclosed Income & Asset

This category applies to taxpayers who did not disclose their overseas income or asset and, consequently, did not pay the applicable tax.

• Threshold: Applicable for undisclosed income/assets up to ₹1 Crore.

• Cost to Taxpayer:

◦ 30% Tax on the Fair Market Value (FMV) of the asset or undisclosed income.

◦ 30% Additional Income Tax (in lieu of penalty).

• Benefit: Immunity from prosecution under the Black Money Act.

Category B: Disclosed Income but Undisclosed Asset

This applies to taxpayers who disclosed the income (e.g., paid tax on dividends or capital gains from foreign shares) but failed to declare the asset itself in the ITR (Schedule FA). This is treated as a technical reporting default.

• Threshold: Applicable for asset values up to ₹5 Crore.

• Cost to Taxpayer: A flat fee of ₹1 Lakh.

• Benefit: Immunity from both penalty and prosecution.

Additional Relief: Retrospective Immunity for Assets < ₹20 Lakh

Apart from FAST-DS 2026, the Budget proposes a permanent amendment to the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015.

• The Change: Prosecution provisions will not apply to failure to disclose non-immovable foreign assets (like bank accounts or shares) if the aggregate value is less than ₹20 Lakh,.

• Effective Date: This immunity is retrospective, effective from 1st October 2024,.

Why Is This Important?

Previously, the Black Money Act imposed severe penalties (₹10 lakh) and prosecution even for minor lapses, such as failing to report a foreign bank account with a negligible balance. The FAST-DS 2026 and the ₹20 lakh immunity threshold distinguish between “small taxpayers” and “large evaders,” ensuring that students and employees are not treated as criminals for inadvertent lapses,.

Note: Cases involving proceeds of crime or where prosecution has already been initiated may be excluded from the scheme.

Disclaimer: The content above is based on the proposals contained in the Finance Bill, 2026 and Budget documents. The scheme will come into force from a date to be notified by the Central Government.